Get Credit Limit up ₹5 Lakhs ✔️₹500 Amazon Voucher

Apply NowGet a credit card no matter what your salary may be. Simply apply for a credit card after reading all the terms and conditions and you will get one in no time. Your salary is no longer a hindrance when it comes to getting the best features out of a credit card. Unlock a world of benefits with any credit card, no matter your salary.

Easily calculate your monthly EMIs for credit card purchases with Airtel Finance. Enter the amount, tenure, and interest rate to get instant estimates.

Applying for a credit card is easy. Follow the steps below:

Download the app and go to Shop section

Click on the credit card banner

Now fill up the complete application form

The card will be delivered to you very soon

Fulfill these eligibility criteria to get the Credit Card!

Individual should be a Resident of India

Age of the primary cardholder should range between 18 and 70 years.

PAN card or Form 60, Residential, Identity, and Income proof, Colour Photograph

There are no credit cards you can directly apply for a salary of 5000 or below. but with this salary range, you can apply for credit cards without income proof.

Simply apply for a secured credit card and enjoy all the benefits of any regular credit card. Here are some of the best-secured credit cards:

| Card Name | Features | Benefits |

| SBI Advantage Plus | Credit limit up to 85% of FD amount Extended credit with 2.25% interest Cash withdrawal up to 100% of credit limit ‘Easy Money’ facility Credit transfer from other cards Encash facility | Use at 1 million+ Visa/MasterCard ATMs globally Convert transactions to EMIs Interest on FD after 555 days Supplementary card benefits |

| Axis Insta Easy | Withdraw up to 100% of credit limit Credit limit up to 80% of FD 1% fuel surcharge waiver | 15% discount on dining Platinum chip Convert transactions over Rs.2,500 to EMIs |

| SBI ELITE | Use at 24 million+ outlets worldwide Save up to 1% on fuel Add-on cards for family Global card replacement Fraud liability cover of Rs.1 lakh | Welcome gift voucher of Rs.5,000 5x reward points on groceries, dining, departmental stores 2 reward points per Rs.100 spent Complimentary movie tickets worth Rs.6,000/year Access to 2 domestic and 6 international airport lounges 50,000 bonus points worth Rs.12,500/year 10,000 bonus points for Rs.3 lakh or Rs.4 lakh spend/year |

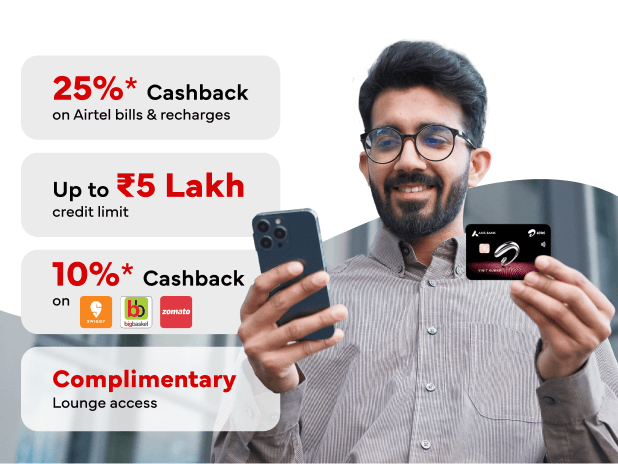

10% cashback on food & groceries, 25% on Airtel bills, and high card limit up to ₹5,00,000. Bonus: Get ₹500 Amazon voucher after first use.