Instant Credit Limit

₹900000*

ACTIVATE NOW

Get Flexi Credit up to ₹10 lakhs ✔️Instant disbursal ✔️100% online process

Apply NowA dry loan is a term used in real estate transactions, referring to a situation where the loan funds are not immediately disbursed at the time of closing. Instead, the disbursement takes place after all the necessary paperwork has been completed and thoroughly reviewed by the lender. This concept, often called a "dry closing," can vary significantly from one region to another, depending on local regulations.

In India, the term "dry loan" may be less commonly used, but it relates closely to the principles of certain types of loans where disbursement processes are structured similarly.

Essentially, in a dry loan scenario, a buyer and seller may complete the closing formalities while the actual transfer of funds is delayed. This process ensures that all documentation is accurate and compliant, reducing the risk of fraud or errors. The funds become "dry" as they are not accessible until the necessary checks are finalised, typically taking several days post-closing.

Key characteristics of dry loans include:

Opting for a dry loan has several advantages, particularly for buyers and lenders:

To be eligible for a dry loan in India, borrowers must meet certain criteria set by the lending institution. These requirements ensure that the borrower is financially stable and capable of repaying the loan. Some common eligibility criteria include:

A dry loan offers several distinct features that set it apart from other types of loans in the real estate financing space. One of the most notable characteristics is the delayed fund disbursement. In a dry loan, the lender releases the funds only after all required documentation has been completed and thoroughly reviewed. This additional layer of security benefits both the buyer and the lender by ensuring that all legal and financial aspects of the transaction are in order before any money changes hands.

Due to the comprehensive paperwork validation process, the closing process for a dry loan is typically longer compared to other loan types. This increased processing time allows for a more thorough review of all documents, providing legal assurance that there are no outstanding issues or disputes regarding the property. Dry loans can be structured as either fixed-rate or adjustable-rate mortgages, giving borrowers some flexibility in choosing the best financial product for their needs.

By not providing immediate funds at closing, dry loans offer a form of risk management. The delay allows more time to address any potential issues that may arise during the transaction process, thereby minimising risks associated with property purchases. It is important to note that the legality and procedures surrounding dry loans can vary by region, so potential borrowers should be aware of local laws and practices related to dry funding in their area.

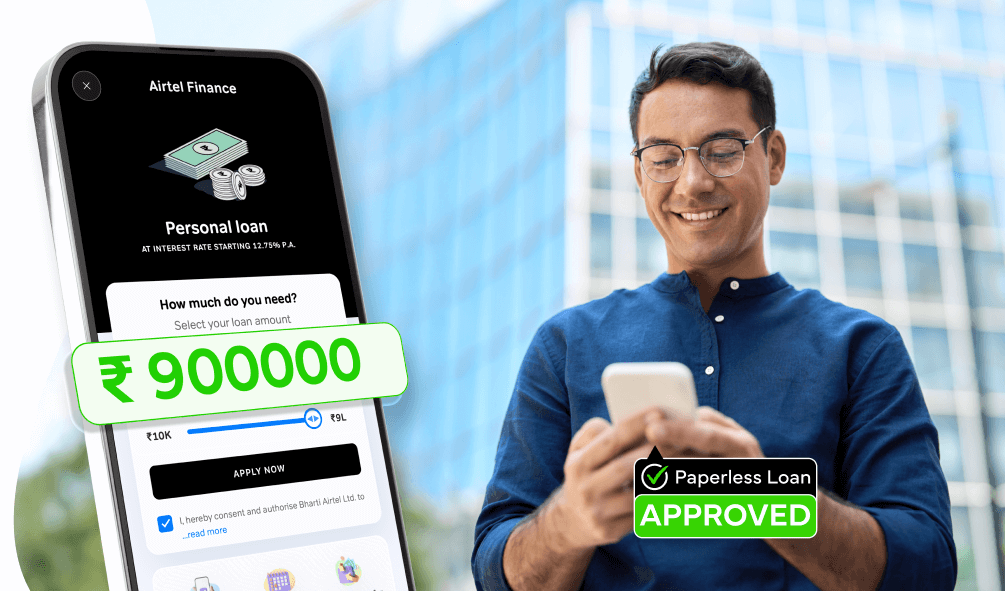

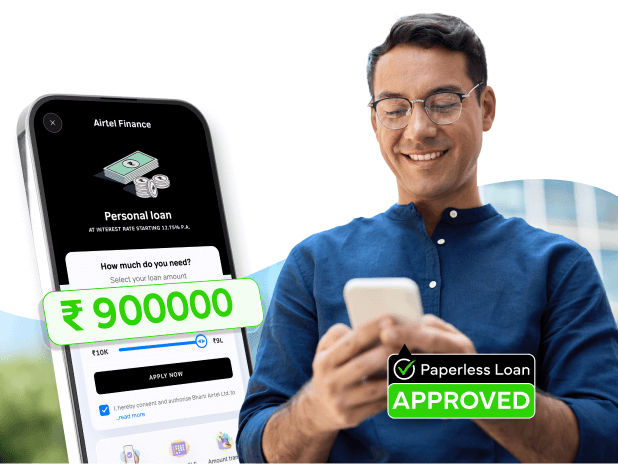

Applying for a dry loan with Airtel Finance is a straightforward process designed to provide you with quick access to funds. Here's a step-by-step guide on how to apply:

When it comes to choosing a financial services provider, Airtel Finance stands out for several reasons:

By choosing Airtel Finance for your dry loan requirements, you can rest assured that you are partnering with a trusted and reliable financial services provider committed to your financial well-being.

Fast approval for medical, travel or urgent payments.