Instant Credit Limit

₹1000000*

ACTIVATE NOW

Get Flexi Credit up to ₹10 lakhs ✔️Instant disbursal ✔️100% online process

Apply NowWhen it comes to buying a home, most people think of taking out a mortgage or a home loan. However, personal loans can also play a role in the home-buying process, albeit indirectly. Personal loans are a type of unsecured credit that can be used for various purposes, including debt consolidation, medical expenses, or unexpected events.

While personal loans are not typically suited for purchasing a house outright due to their limited loan amounts and higher interest rates, they can still be useful in supporting the broader home-buying process. In the Indian subcontinent, personal loans usually range from ₹1 lakh to ₹50 lakhs, which is insufficient for buying the average Indian home, with prices often exceeding ₹20 lakhs in urban areas.

Moreover, personal loans have higher interest rates compared to home loans, typically ranging from 10% to 24% per annum, making them less affordable for major purchases like a house. However, personal loans can be used to consolidate debt or cover smaller expenses related to home purchasing, such as renovations or moving costs.

For significant home-related expenses, other options like home loans or home equity loans might be more suitable due to their lower interest rates and larger loan amounts. Nevertheless, taking a personal loan and repaying it responsibly can positively impact your credit score, which is beneficial when applying for a mortgage.

While personal loans are not typically used for purchasing full-sized homes due to limited loan amounts, they can be beneficial in certain scenarios, such as buying tiny homes or manufactured homes. Let us read about some of them:

No collateral required

Personal loans are unsecured, eliminating the need for property or asset pledges. This reduces risk, as defaulting won’t lead to losing your home, unlike secured loans.

Quick disbursal

Approval and funding often occur within days, unlike mortgages that take weeks. Ideal for urgent needs like down payments or time-sensitive purchases.

Flexible usage

Funds can cover various expenses—land purchases, renovations, or even stamp duty—without lender restrictions tied to specific home loan purposes.

Simplified process

Minimal documentation (income, ID, and address proof) speeds up approval, avoiding lengthy property verifications required for mortgages.

No prepayment penalties (Often)

Many lenders allow foreclosure without extra charges, helping you save on interest if repaid early.

Fixed repayment schedule

EMIs remain constant throughout the tenure, aiding budget planning without floating-rate uncertainties common in home loans.

Credit score boost

Timely repayments improve your credit history, enhancing eligibility for future loans (e.g., mortgages) at better terms.

No end-use monitoring

Lenders don’t track fund usage, offering freedom to allocate money as needed—unlike home loans tied to construction stages.

However, it's important to note that personal loans usually have higher interest rates than mortgages, and their interest is not tax-deductible. If you're considering a personal loan for home buying, it's essential to understand the application process.

Applying for a personal loan involves several steps. Let us go through them:

An EMI calculator is an essential tool for understanding your monthly repayment amount when taking out a personal loan for home buying. You can use online tools available on most lenders' websites to calculate your EMI based on the loan amount, interest rate, and tenure.

Here are the key factors to consider when using an EMI calculator:

By entering these details into an EMI calculator, you can determine the exact monthly payment required to repay your loan. For example, let's say you borrow Rs.50,000 at an interest rate of 12% for 2 years. Using an EMI calculator will provide the monthly payment amount based on these inputs.

If you're considering a personal loan for home buying in India, it's essential to understand the key features of these loans. One significant advantage is their unsecured nature, meaning you don't have to put up your property as collateral.

However, this also means that the borrowing amounts are typically lower than mortgages, ranging from Rs.50,000 to Rs.50 lakhs, depending on your creditworthiness and the lender.

On the bright side, personal loans often have faster funding times compared to mortgages, with funds available within a few days. The repayment terms are also shorter, ranging from 12 to 60 months, which means higher monthly payments but quicker loan repayment.

Keep in mind that personal loan interest rates are higher than mortgages, and the interest is not tax-deductible. One of the most attractive features of personal loans is their flexibility in usage. You can use them for various purposes related to home buying, such as:

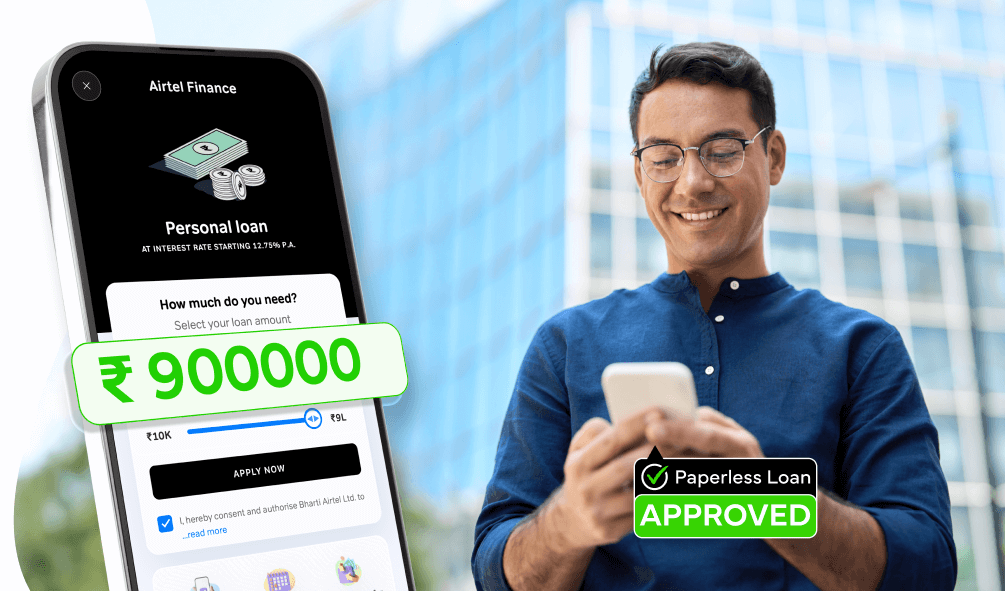

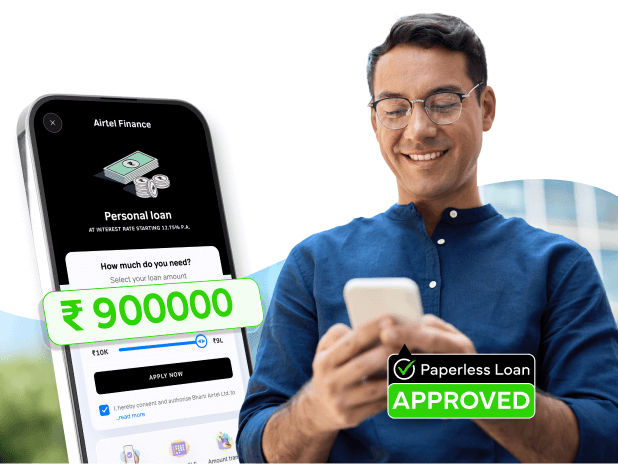

Airtel Finance prioritises speed and convenience, offering instant disbursal directly to your bank account. The competitive edge lies in providing one of the lowest interest rates, starting at just 12.75%, ensuring affordability.

You can access a substantial loan amount, with limits reaching up to ₹10 lakhs, catering to a wide range of financial requirements. Furthermore, we've streamlined the process to be completely paperless, saving you time and hassle. Choose Airtel Finance for a seamless and efficient loan experience.

Fast approval for medical, travel or urgent payments.