Check Your Credit Score for FREE

Know your CIBIL score instantly and understand your loan & card eligibility in seconds. ₹399 ₹0

✔ Verified Report

⏱ 2 Min Check

⚡ No Impact on Score

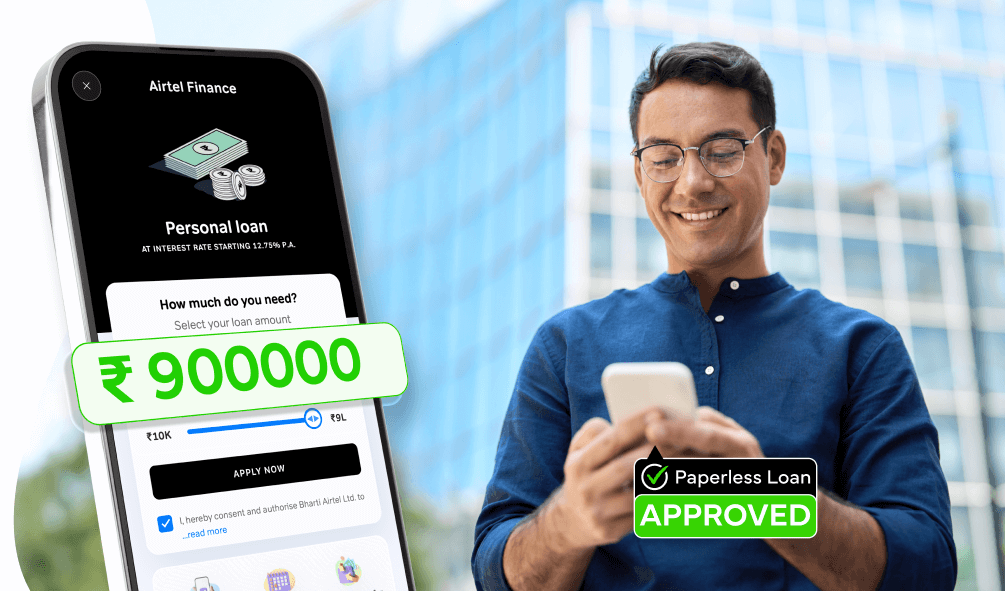

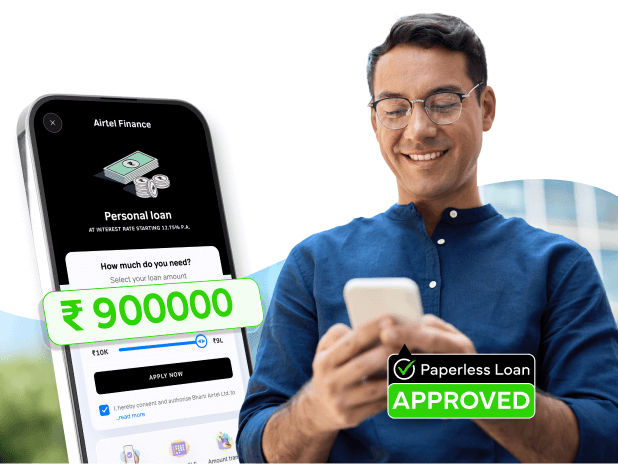

Get Flexi Credit up to ₹10 lakhs ✔️Instant disbursal ✔️100% online process

Check NowA CIBIL score is a three-digit number ranging from 300 to 900 that represents your creditworthiness. Generated by the Credit Information Bureau (India) Limited, this score is calculated based on your credit history, repayment patterns, and overall financial behaviour. Lenders use this score to assess the risk of lending money to you, making it one of the most important financial tools in India today.

Your CIBIL score directly impacts your financial opportunities. A good score opens doors to better loan terms, lower interest rates, and faster approvals for credit cards, personal loans, home loans, and other financial products. It's essentially your financial report card that banks and NBFCs use to determine whether you are a reliable borrower. Without a healthy CIBIL score, you might face loan rejections or be offered credit at higher interest rates.

Checking your CIBIL score has never been easier with Airtel Finance. Here's how you can access your free credit report worth ₹500:

The entire process takes less than 2 minutes, and you can check your score monthly to stay updated on your credit health.

Understanding your CIBIL score range helps you know where you stand financially:

|

CIBIL Score Range |

Category |

Meaning |

|

750 – 900 |

Excellent |

Highest approval chances with the best interest rates. |

|

700 – 749 |

Good |

Good approval chances with competitive interest rates. |

|

650 – 699 |

Fair |

Moderate approval chances; loan terms may require negotiation. |

|

600 – 649 |

Poor |

Limited loan options with higher interest rates likely. |

|

300 – 599 |

Very Poor |

Loan approval is difficult; focus on improving your credit score. |

Most lenders prefer scores above 700, while scores above 750 are considered excellent and can help you negotiate better terms.

CIBIL score calculation involves multiple factors that reflect your credit behaviour:

The CIBIL score calculation algorithm processes this data to generate your final score, which gets updated regularly based on fresh information from lenders.

Lenders check your CIBIL score to minimise their risk when offering credit. Your score provides them with a quick snapshot of your creditworthiness without having to manually review years of financial history. It helps them decide loan approval, determine interest rates, and set credit limits. A good CIBIL score signals that you're a responsible borrower who pays back on time, making lenders more confident about approving your application.

Maintaining a good CIBIL score offers numerous financial advantages:

Several factors can negatively impact your CIBIL score:

If you don't have a CIBIL score, it means you haven't used formal credit products yet.

Improving your CIBIL score requires consistent financial discipline and time:

To boost your credit score, follow these practical tips:

After checking your free credit report on Airtel Finance, analyse your score and identify areas for improvement. If your score is good, you can confidently apply for loans or credit cards with better terms. For lower scores, create an action plan to address the issues mentioned in your credit report. Consider speaking with financial advisors if you need help understanding complex credit issues, and most importantly, make checking your CIBIL score a monthly habit to track your progress.

Many people worry unnecessarily about factors that don't impact CIBIL score calculation. Your salary amount, savings account balance, and investment portfolio don't directly affect your score. Age, marital status, and employment designation also don't influence the calculation. Checking your own CIBIL score multiple times doesn't hurt your score either. Focus on the factors that actually matter: payment history, credit utilisation, and responsible credit behaviour.

It will take 2 mins and is absolutely free. We promise!

Check your Free Credit ReportKnow your CIBIL score instantly and understand your loan & card eligibility in seconds. ₹399 ₹0