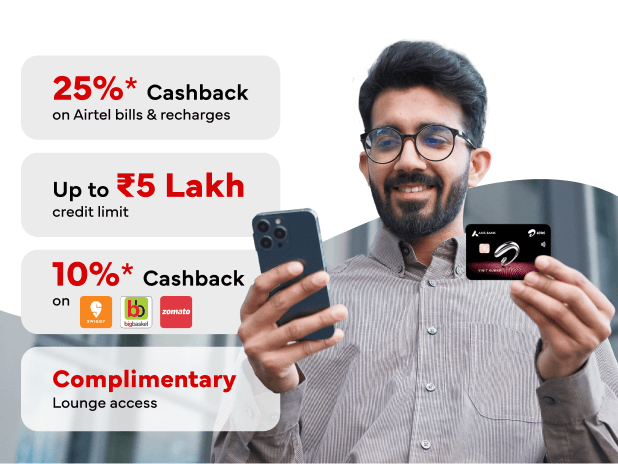

Get Credit Limit up ₹5 Lakhs

Apply NowGetting a regular credit card can be difficult if you’re new to credit or rebuilding your profile. A credit card against a fixed deposit offers a simple and reliable alternative. With Airtel Finance, you can use your existing fixed deposit as security to get a credit card, making approval easier while continuing to earn interest on your FD.

A credit card against FD is a secured credit card issued by placing a lien on your fixed deposit. Your FD remains active and continues earning interest while it acts as collateral for the credit card.

The credit limit is linked to the FD amount, and regular card usage with timely repayments helps build a positive credit history. If dues are not cleared, the bank may adjust the outstanding amount against the fixed deposit, as per applicable terms. This option is especially useful for first-time credit users or those looking to strengthen their credit profile, as approval is primarily based on the fixed deposit rather than income or credit score.

Credit cards offer several valuable features and perks. Some of the key credit card benefits include:

*T&C apply .

Easily calculate your monthly EMIs for credit card purchases with Airtel Finance. Enter the amount, tenure, and interest rate to get instant estimates.

Airtel Finance offers an FD-based credit card designed for individuals who want easier access to credit using a fixed deposit as security.

This FD-backed credit card is ideal for first-time cardholders or those rebuilding credit, as approval is linked to the FD rather than income or past credit score. The fixed deposit continues to earn interest while supporting your credit limit, offering a secure and convenient way to use a credit card.

To apply for a credit card against a fixed deposit through Airtel Finance, you need to meet the following basic eligibility criteria:

A credit card against a fixed deposit is well-suited for individuals looking for easy and secure access to credit. It is especially useful for:

Applying for a credit card against a fixed deposit through Airtel Finance is a simple and secure process. Since the card is backed by your FD, approval is easier and does not depend heavily on your credit history.

Step 1: Check Basic Eligibility

You must be an Indian resident with a valid fixed deposit. The FD amount and tenure should meet the issuing bank’s minimum requirements.

Step 2: Apply Digitally

You can apply through the Airtel Thanks App or the partner bank’s official digital platform by selecting the FD-backed credit card option and entering your basic details.

Step 3: FD Verification and Card Issuance

Once your fixed deposit details are verified and KYC is completed, the credit card is issued against the FD value as per applicable terms.

The best credit cards against fixed deposit options often come with additional benefits like reward points and cashback offers, making this an attractive choice for building credit responsibly.

Understanding the differences between an FD-based credit card and regular credit cards helps you make an informed decision about which option suits your financial needs better.

|

Feature |

Credit Card Against Fixed Deposit |

Regular Credit Card |

|

Approval basis |

Issued against a fixed deposit held as security |

Based on income, credit score, and repayment history |

|

Credit limit |

Linked to the FD value |

Determined by income and credit profile |

|

Collateral required |

Yes, fixed deposit is pledged |

No collateral required |

|

Interest on FD |

FD continues to earn interest |

Not applicable |

|

Documentation |

Minimal, as FD acts as security |

Income and credit-related documents required |

|

Credit history requirement |

Suitable for no or limited credit history |

Requires established credit profile |

|

Risk level for issuer |

Lower due to secured nature |

Higher as it is unsecured |

Choose a credit card against FD if you're new to credit, have a low credit score, or want guaranteed approval. Regular credit cards suit those with established credit histories seeking higher limits and premium benefits. The FD-based credit card approach offers a perfect stepping stone to build creditworthiness while maintaining the security of your savings.

Earn up to 25% cashback on Airtel Mobile, Broadband & DTH recharges through Airtel App.

*T&C apply