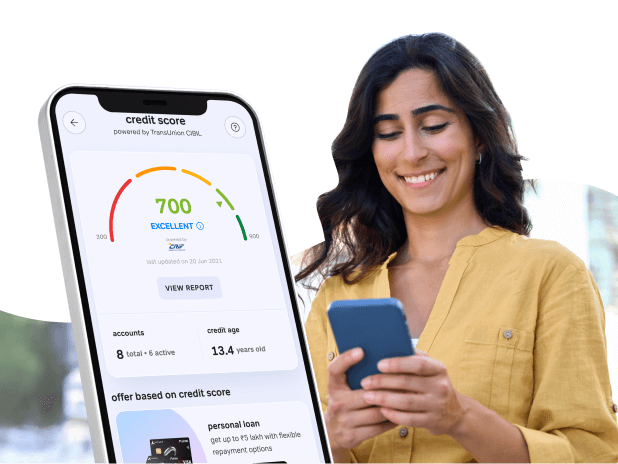

Check Your Credit Score for FREE

Know your CIBIL score instantly and understand your loan & card eligibility in seconds. ₹399 ₹0

✔ Verified Report

⏱ 2 Min Check

⚡ No Impact on Score

Get Flexi Credit up to ₹10 lakhs ✔️Instant disbursal ✔️100% online process

Check Now

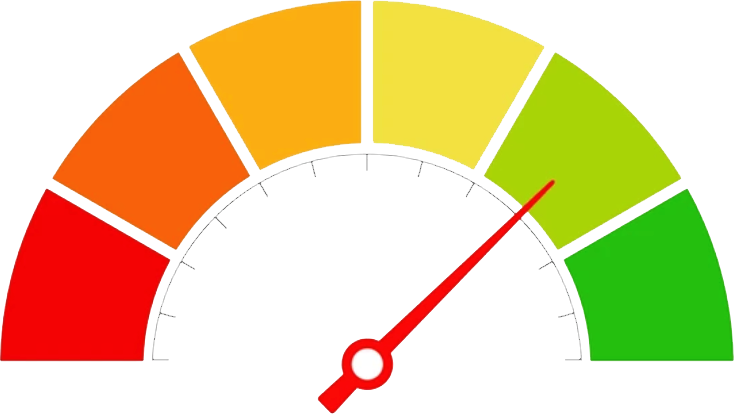

The credit score is a three-digit figure that ranges from 300 to 900, indicating your creditworthiness, or ability to repay debts. A higher credit score reflects a stronger repayment capacity, while a lower score suggests the opposite.

When applying for a personal loan, your credit score is a crucial factor. A good score is essential for qualifying for the loan and can also lead to more favorable terms and lower interest rates.

| CREDIT SCORE/CIBIL SCORE RANGE | WHAT IT DENOTES |

|---|---|

| Less Than 650 | Poor – This indicates quite a lot of credit issues and you may need to take a good look to improve it for favourable outcomes |

| 650-699 | Average – This is close to reaching a good credit score but needs improvement |

| 700-749 | Good – This indicates a responsible credit history which may get you favourable interest rates |

| 750-849 | Great – This score shows consistency in repayment and a very good history with no defaults or penalties |

| 850-900 | Excellent – This means you are eligible for all kinds of loans because your credit history is Excellent |

Your credit score is calculated by authorized credit agencies such as TransUnion CIBIL, Equifax, and Experian. It is based on your credit history, which reflects how you have managed and repaid credit in the past.

If you have a long credit history and consistently made timely payments, you'll likely have a good credit score, making it easier to secure a personal loan with favorable terms.

Conversely, if you've missed payments or been late in repaying, your credit score will be lower. This could result in your loan application being rejected or being offered a loan at higher interest rates.

Understand what affects your credit score and how it's calculated. Perfect for beginners.

Learn MoreLearn what affects your credit score and how to improve it step-by-step.

Learn MoreDiscover the key factors banks and lenders examine in your credit report before approving your loan.

Learn MoreLearn how credit scores and CIBIL scores differ and why both matter for your financial journey.

Learn MoreStep-by-step guide for people with no credit history to build a strong credit profile.

Learn MorePro tips for optimizing your credit profile and maximizing your financial opportunities.

Learn MoreMake sure you have a good credit score and then getting credit becomes extremely easy.

Factors that affect credit score are as follows :

| Payment history | This is the most important factor, and it accounts for about 35% of your score. Banks or lenders want to see that you have a history of making your payments on time. |

| Amounts owed | It accounts for about 30% of your score. Make sure that you are not using too much of your available credit. |

| Length of credit history | Accounts for about 15% of your credit score, where you have to show that you have a long history of using credit responsibly. |

| New credit | This factor accounts for about 10% of your score, where lenders want to see that you are not applying for too much new credit at once. |

| Types of credit | Accounting about 10% of your credit score, banks or lenders want to see that you have a variety of credit accounts, such as credit cards and loans. |

There are many benefits to having a good credit score. Here are a few of the most important ones:

Lenders check your CIBIL score for several reasons. Listing out the reasons for you to discover the best tricks.

| Reason | Description |

|---|---|

| Assess Creditworthiness | Shows if you can repay based on past credit behavior. |

| Evaluate Risk | Higher scores mean less risk; lower scores indicate trouble. |

| Make Loan Decisions | Key factor in approving or denying loan applications. |

| Set Interest Rates | Affects the interest rate; better scores often get lower rates. |

| Determine Credit Limits | Helps decide how much credit you can get on loans or cards. |

| Prevent Fraud | Confirms your identity and spots potential fraud. |

A low CIBIL score can arise from various factors:

| Missed Payments | High Credit Utilization |

| Limited Credit Mix | Short Credit History |

| Frequent Hard Inquiries | Defaults/Bankruptcies |

Improving the credit score is important for accessing better loan terms, lower interest rates, and increased financial opportunities.

Some effective ways to help you boost your credit score:

| Method | Description |

|---|---|

| Pay Bills on Time | Ensure all loan and credit card payments are made on time. |

| Reduce Credit Utilization | Keep usage below 30% of your total credit limit. |

| Diversify Credit Mix | Have a variety of credit accounts (credit cards, loans). |

| Check Your Credit Report | Regularly review for errors and dispute inaccuracies. |

| Limit New Credit Applications | Avoid applying for multiple accounts at once. |

| Keep Old Accounts Open | Maintain older accounts to lengthen your credit history. |

| Set Up Payment Reminders | Use reminders or automatic payments for timely payments. |

| Work with a Credit Counselor | Seek advice from a credit counseling service if needed. |

It will take 2 mins and is absolutely free. We promise!

Check your Free Credit ReportKnow your CIBIL score instantly and understand your loan & card eligibility in seconds. ₹399 ₹0