Extremely flexible

Airtel Flexi Credit is quite flexible. You can easily choose the personal loan amount, loan tenure and EMI.

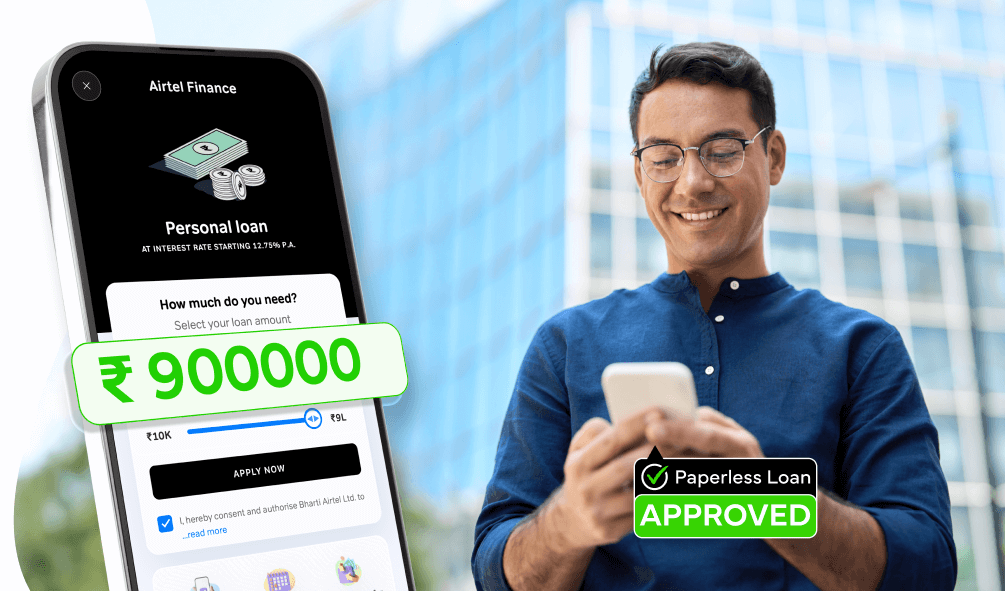

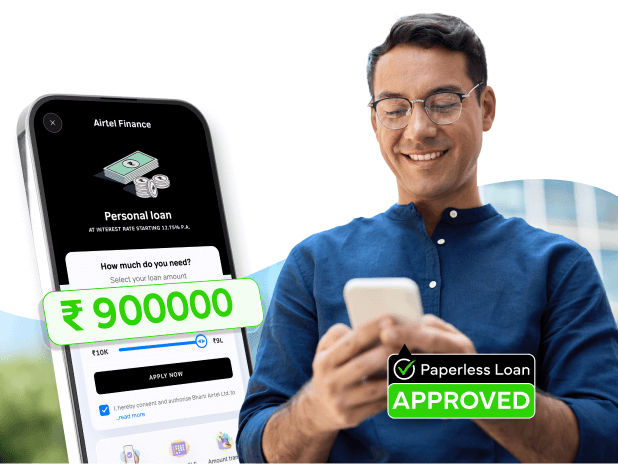

Get Flexi Credit up to ₹10 lakhs ✔️Instant disbursal ✔️100% online process

Apply Now

To calculate the interest rate on your education

loan amount, simply multiply the principal amount

by the interest rate and the time period, in years.

The formula is- Interest = A – P Wherein,

A = Total amount paid

P = Principal amount paid

R = Rate of interest

T = Number of years

Discover how our personal loans can be tailored to meet your specific needs. Whether you need a personal loan online for travel, education, emergencies, or any other purpose, find the right loan option that fits your unique situation.

With Airtel Flexi Credit, high-interest rates are a story from the past!

Airtel Flexi Credit is quite flexible. You can easily choose the personal loan amount, loan tenure and EMI.

Apply for the Airtel Flexi Credit through a simplified process.

Starting at just 11.5% per annum, Airtel Finance provides personal loans at the most competitive rates.

Follow the simple steps mentioned below

Find Shop > Airtel Finance

Fill in your basic details

Basis profile verification

Link your bank account

With Airtel Flexi Credit, you get

₹10,000 to ₹10,00,000

Starting from 11.5% p.a.

03 to 60 months

Within 24 hours

No paperwork

2% to 4% + GST

Applying for a Airtel personal loan has never been easier. Follow these simple steps to quickly complete your application and get your loan disbursed directly into your bank account.

Education loan interest rates are the charges incurred by banks or financial institutions for lending you money to pursue your education. In other words, it is the fees you pay to the banks or lenders to provide you with the education loan. This interest rate may vary from loan to loan. However, for an education loan, the interest rate depends on your credit history, lending policies, market conditions, and loan repayment terms. The higher the education loan interest rate, the more you pay the loan fees.

Fast approval for medical, travel or urgent payments.

Get a personal loan with minimal documentation from Airtel Finance

Apply Now