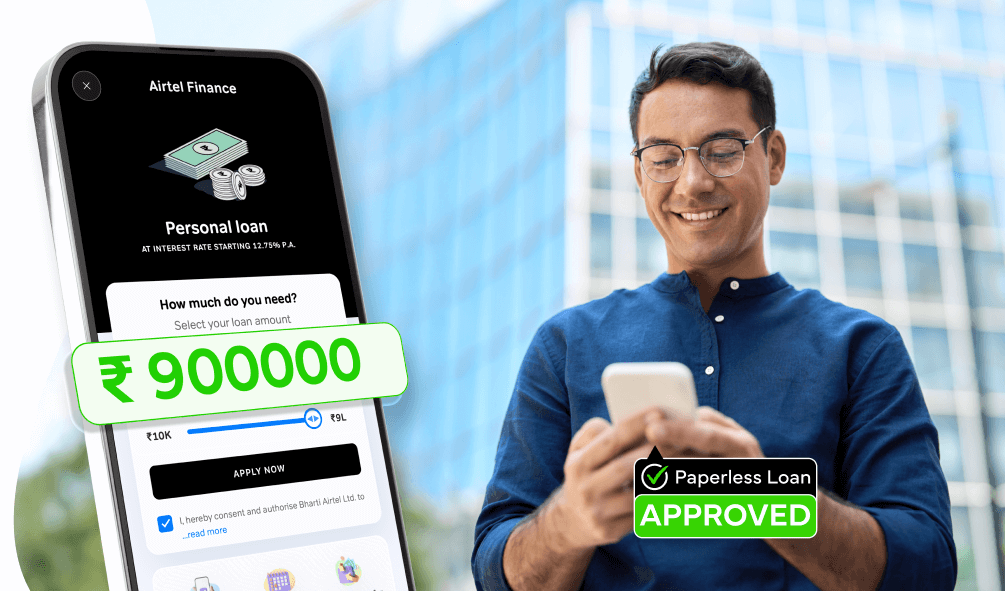

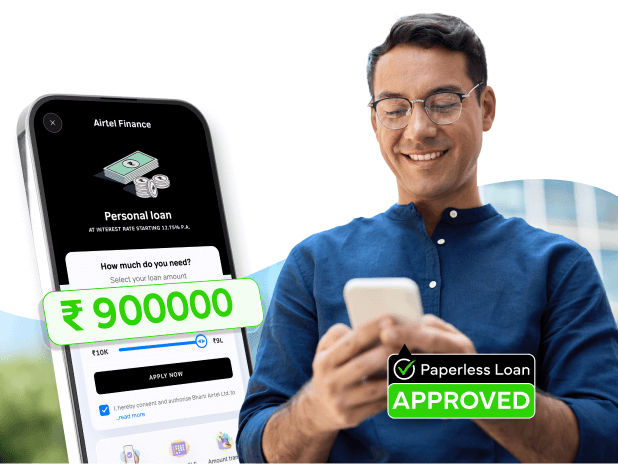

Get Flexi Credit up to ₹10 lakhs ✔️Instant disbursal ✔️100% online process

Apply Now

Understanding personal loan interest rates is crucial when you are planning to borrow money for urgent needs, medical emergencies, or planned expenses like weddings. Interest rates directly impact your monthly EMI and total repayment amount, making it essential to compare rates across different lenders. While traditional banks may offer varying rates based on multiple factors, digital lending platforms, through partnerships with established NBFCs, provide transparent, competitive rates with quick processing.

When comparing options like L&T Finance personal loan interest rates with other lenders, focus on the Annual Percentage Rate (APR) rather than just the advertised interest rate, as APR includes all charges and gives you the true cost of borrowing.

The Marginal Cost of Lending Rate (MCLR) is the minimum interest rate below which banks cannot lend. This rate is determined by factors including the cost of funds and operating expenses. MCLR rates are reviewed monthly by banks and directly influence personal loan interest rates. Currently, major banks have MCLR rates ranging from 8.5% to 9.5% annually. However, personal loans are typically offered at rates significantly higher than MCLR, as they are unsecured loans with a higher risk. Digital lending platforms often work with multiple lending partners, allowing them to offer competitive rates that may be more attractive than traditional bank offerings.

Discover how our personal loans can be tailored to meet your specific needs. Whether you need a personal loan online for travel, education, emergencies, or any other purpose, find the right loan option that fits your unique situation.

APR represents the true cost of borrowing, including interest rates and additional fees. Unlike the basic interest rate, APR gives you a comprehensive view of what you will actually pay. For instance, if a lender advertises 12% interest but charges a 2% processing fee, your effective APR might be 13-14%.

APR helps you compare different lenders fairly. A loan with 15% interest and no processing fee might be cheaper than one with 12% interest and a 3% processing fee when you calculate the APR. Digital lending platforms often provide transparent APR calculations upfront, helping you understand the complete cost before committing to a loan.

Your interest rate directly impacts your monthly EMI and total repayment amount. A 2% difference in interest rate on a ₹5 lakh loan over 3 years can save or cost you approximately ₹15,000-20,000. This makes rate comparison crucial for your financial health.

Beyond the financial impact, your interest rate reflects your creditworthiness and borrowing profile. A lower rate indicates strong financial health and a good credit history, while higher rates might signal areas for credit improvement. Understanding these dynamics helps you negotiate better terms and choose the most cost-effective borrowing option.

Personal loan interest is calculated using two main methods: reducing balance and flat rate. Most lenders use the reducing balance method, where interest is calculated on the outstanding principal amount after each EMI payment. This means your interest burden decreases over time.

Lenders consider multiple factors, including your credit score, income stability, employment history, and debt-to-income ratio, when determining your specific rate. Digital lending platforms often use advanced algorithms to assess risk and provide instant rate quotes. The calculation typically starts with a base rate determined by the lender's cost of funds, to which a margin is added based on your risk profile.

Indian lenders primarily use the reducing balance method for personal loans. The formula used is EMI = [P x R x (1+R)^N] / [(1+R)^N-1], where P is principal, R is the monthly interest rate, and N is tenure in months. Under this system, if you borrow ₹1 lakh at 12% annual interest, your first month's interest is ₹1,000 (₹1,00,000 x 12% ÷ 12). After paying your first EMI, the principal reduces, and subsequent interest calculations are on the lower outstanding amount.

Some lenders still use flat rate calculations where interest is calculated on the original principal throughout the loan tenure. This method results in higher effective interest rates, making reducing balance loans more economical for borrowers.

Several key factors influence your personal loan interest rate.

Securing the lowest personal loan interest rate requires strategic preparation and comparison shopping.

Applying for a Airtel personal loan has never been easier. Follow these simple steps to quickly complete your application and get your loan disbursed directly into your bank account.

Fast approval for medical, travel or urgent payments.